Introduction

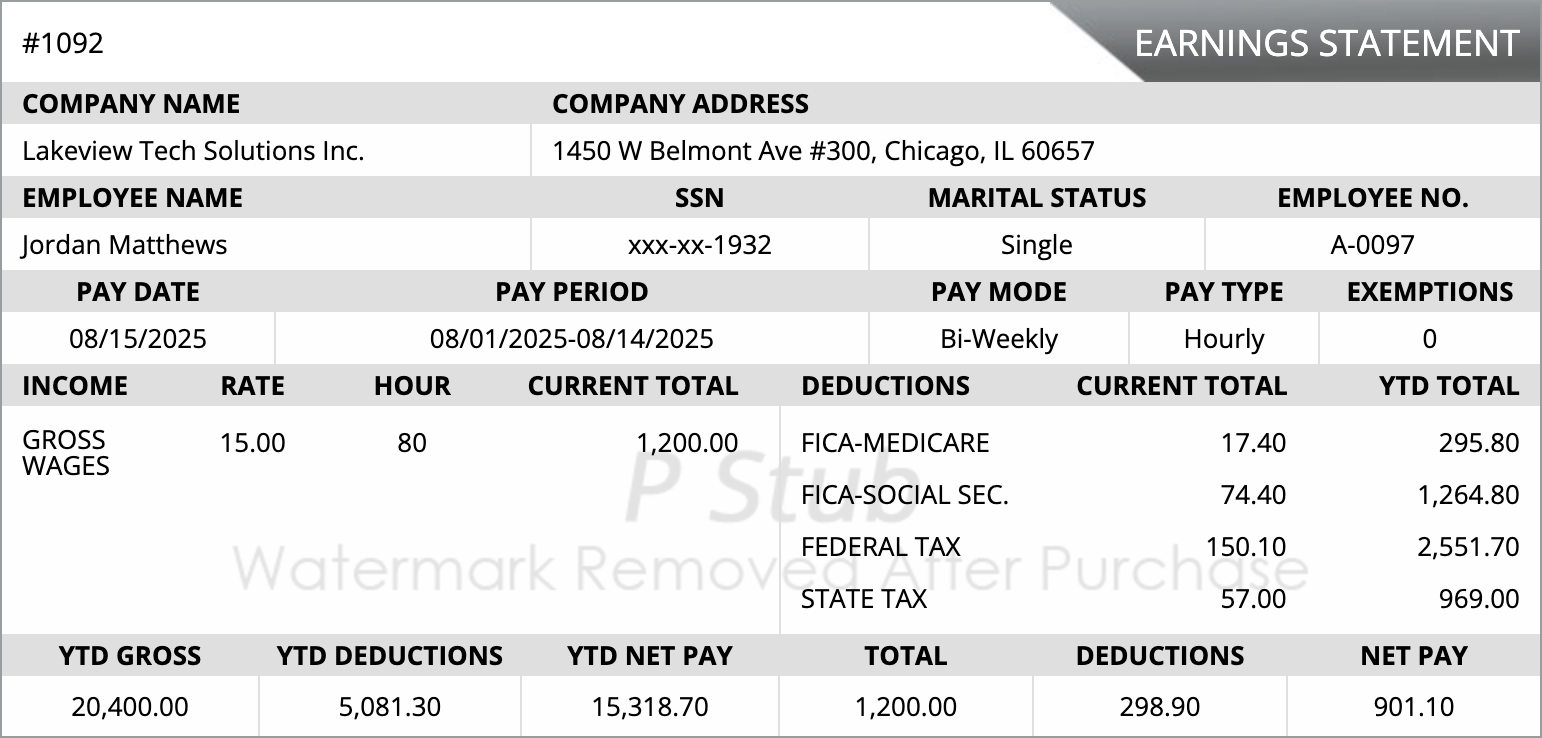

SUTA tax, short for State Unemployment Tax Act tax, is a payroll tax that supports state unemployment insurance programs. These funds help provide temporary income to workers who lose their jobs through no fault of their own. Understanding SUTA tax basics helps employers stay compliant and plan payroll costs accurately.

What Is SUTA Tax?

SUTA tax is a state-level payroll tax paid by employers to fund unemployment benefits. Each state manages its own unemployment insurance program, which means SUTA tax rules, rates, and wage limits vary depending on where the business operates.

Who Pays SUTA Tax?

In most cases, employers are responsible for paying SUTA tax. It is generally not deducted from employee wages. Some states may require employee contributions, but this is less common and depends on state-specific regulations.

How SUTA Tax Is Calculated

SUTA tax calculations are based on two main factors:

- Taxable Wage Base: States set a maximum wage amount per employee that is subject to SUTA tax each year.

- Employer Tax Rate: Employers receive a rate based on factors such as business history and prior unemployment claims, often referred to as an experience rating.

Once an employee’s wages exceed the taxable wage base, no additional SUTA tax is owed for that employee for the remainder of the year.

SUTA vs FUTA

SUTA tax differs from FUTA, the Federal Unemployment Tax Act tax. While both support unemployment programs, SUTA funds state benefits directly, whereas FUTA supports federal oversight and administrative costs. Employers who pay SUTA tax on time may qualify for reduced FUTA liability.

Frequently Asked Questions

Is SUTA tax deducted from employee paychecks?

In most states, SUTA tax is paid entirely by the employer and is not deducted from employee wages.

Does every employer have to pay SUTA tax?

Most employers are required to pay SUTA tax once they meet state thresholds related to wages paid or number of employees.

How often is SUTA tax paid?

SUTA tax is typically reported and paid quarterly through the state unemployment agency.

Can SUTA tax rates change?

Yes. States may adjust employer SUTA tax rates annually based on unemployment claims and overall program funding needs.

Cookies Settings

Cookies Settings Reject All

Reject All Accept All Cookies

Accept All Cookies

Save & Close

Save & Close