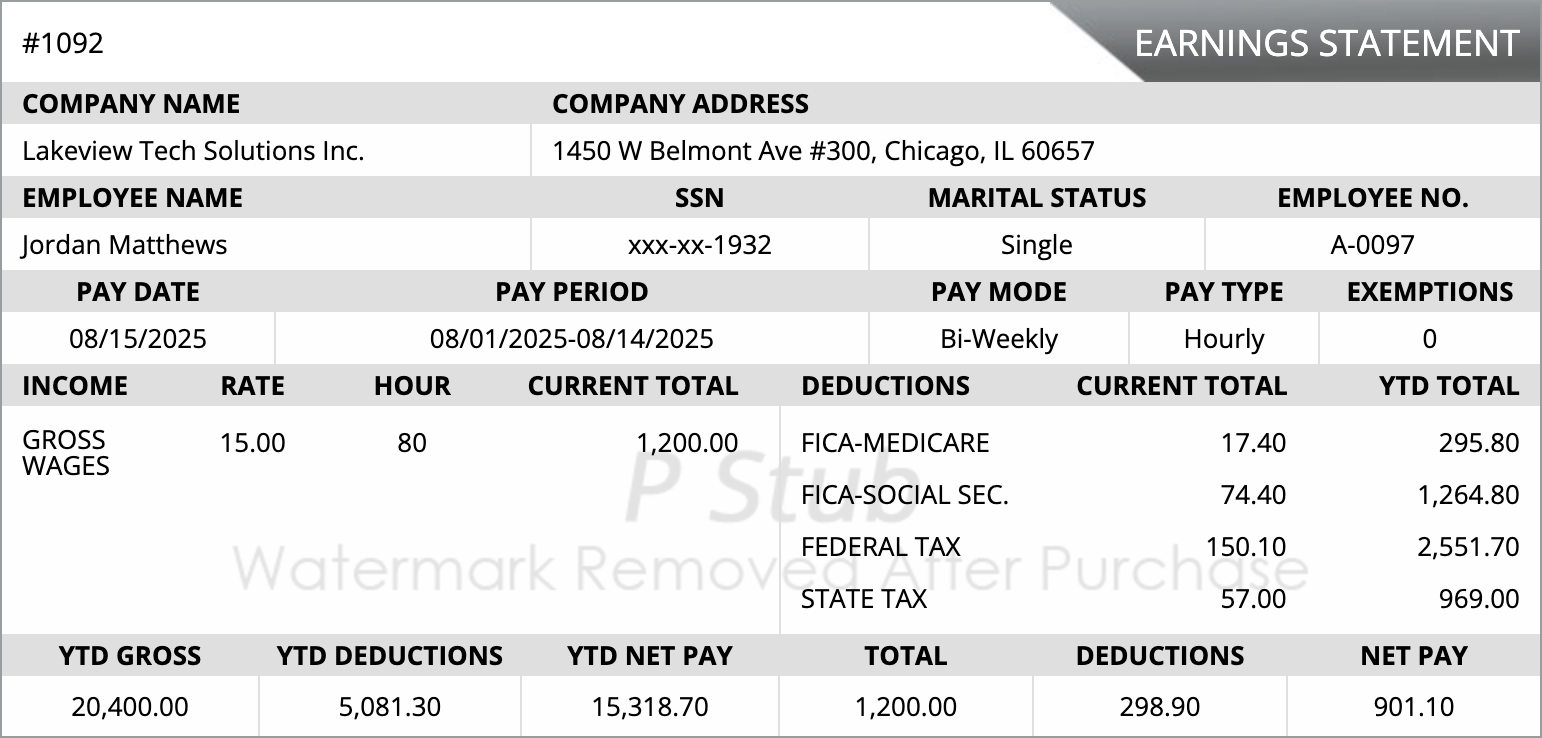

Overview: Pay Stubs as Proof of Income

Pay stubs are official records that document an employee’s earnings, deductions, and net pay for a specific pay period. Employers often provide these as proof of income for loans, rentals, or other financial verification purposes.

Legal Requirements for Pay Stubs

- Many states require employers to provide pay stubs or earnings statements to employees.

- Pay stubs must accurately reflect hours worked, wages, deductions, and taxes.

- Compliance ensures employees have legal documentation for income verification.

Common Uses of Pay Stubs for Verification

- Applying for mortgages, car loans, or personal loans

- Rental or lease applications

- Income verification for government assistance programs

- Personal record-keeping for financial planning

How to Review Pay Stubs for Accuracy

- Check employee information and pay period dates.

- Verify gross earnings match your employment records.

- Review all deductions and tax withholdings for correctness.

- Ensure net pay matches your expected take-home amount.

- Report any discrepancies promptly to HR or payroll.

Frequently Asked Questions

Do employers have to provide pay stubs?

Requirements vary by state, but most employers must provide pay stubs or earnings statements to employees.

Can pay stubs be used for loan applications?

Yes, pay stubs are widely accepted as proof of income for banks, lenders, and rental applications.

What information should a pay stub include?

Employee details, pay period, gross earnings, deductions, taxes, and net pay must all be accurately reported.

How often should I review my pay stubs?

Review every pay stub to ensure accuracy and to catch errors in earnings or deductions promptly.

Use Pay Stubs as Proof of Income Accurately

Ensure your pay stubs are accurate and complete to provide reliable proof of income whenever needed.

Cookies Settings

Cookies Settings Reject All

Reject All Accept All Cookies

Accept All Cookies

Save & Close

Save & Close