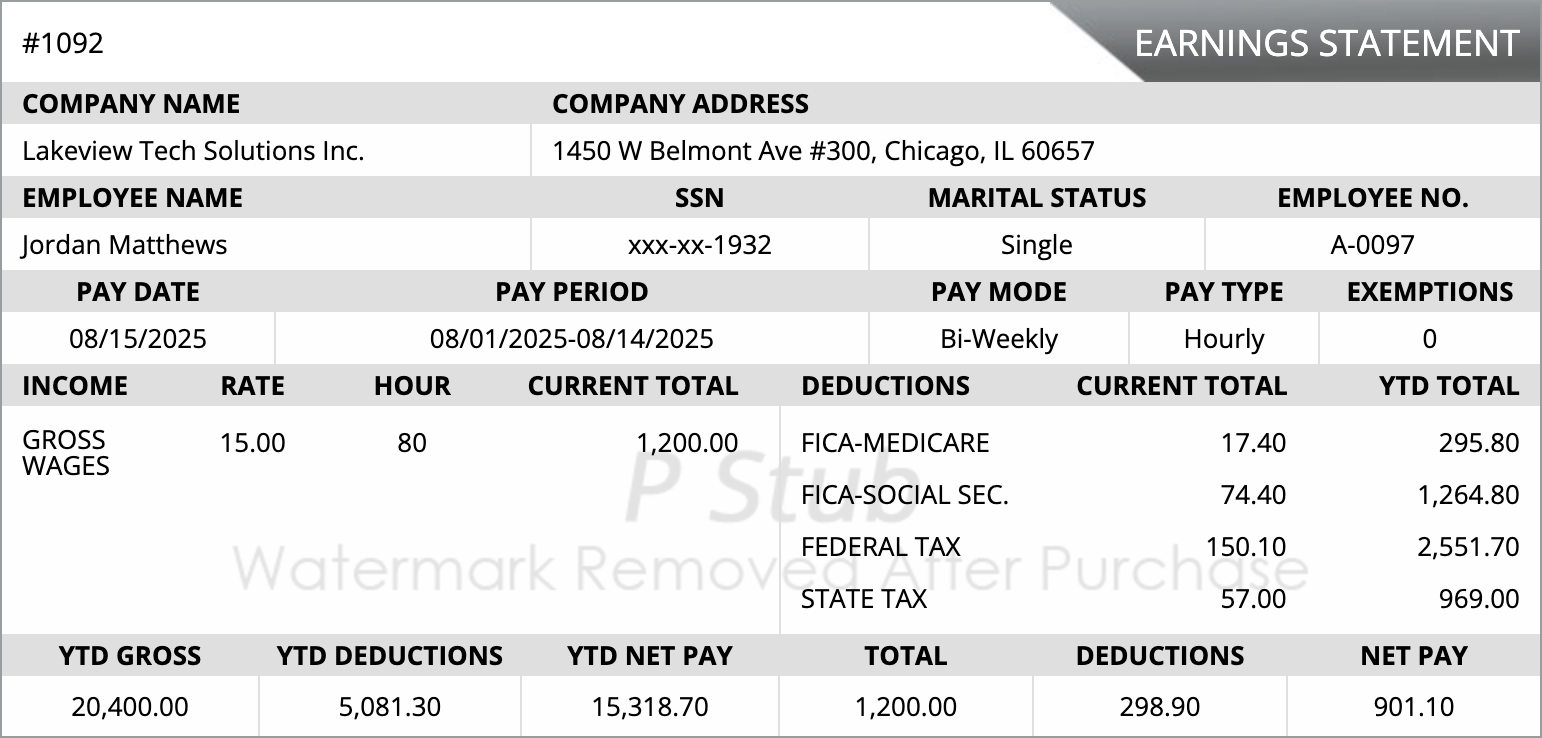

Overview

Calculating your Adjusted Gross Income (AGI) from a paycheck stub is essential for accurate tax filing and financial planning. AGI reflects your total income after certain adjustments and is a key figure for taxes, credits, and deductions.

What Is AGI?

AGI stands for Adjusted Gross Income. It represents your total gross income from wages, salaries, bonuses, and other earnings minus allowable adjustments such as retirement contributions or pre-tax deductions.

Why Calculating AGI Matters

- Determines your federal and state tax liability

- Helps qualify for tax credits and deductions

- Provides a clear picture of your income for financial planning

- Ensures accuracy when filing tax returns

Step-by-Step AGI Calculation from Paycheck Stub

- Locate your gross earnings on the paycheck stub

- Identify pre-tax deductions such as 401(k), health insurance, or HSA contributions

- Subtract these deductions from gross income to calculate your adjusted gross pay

- Sum all adjusted earnings for the year to determine AGI

- Verify totals with year-to-date (YTD) amounts for accuracy

Common Mistakes to Avoid

- Confusing gross pay with adjusted gross income

- Ignoring pre-tax deductions

- Failing to include all income sources

- Not verifying YTD totals

Frequently Asked Questions

Can I calculate AGI from a single paycheck stub?

Yes, but ensure you include all deductions and annualize the income for an accurate AGI.

What deductions should be considered?

Pre-tax contributions such as 401(k), health insurance, and HSA contributions must be subtracted from gross income.

Why is AGI important for taxes?

AGI determines tax liability, eligibility for credits, and certain deductions.

Can freelancers calculate AGI from pay stubs?

Yes, freelancers can use pay records, invoices, and adjusted earnings to determine AGI.

Cookies Settings

Cookies Settings Reject All

Reject All Accept All Cookies

Accept All Cookies

Save & Close

Save & Close