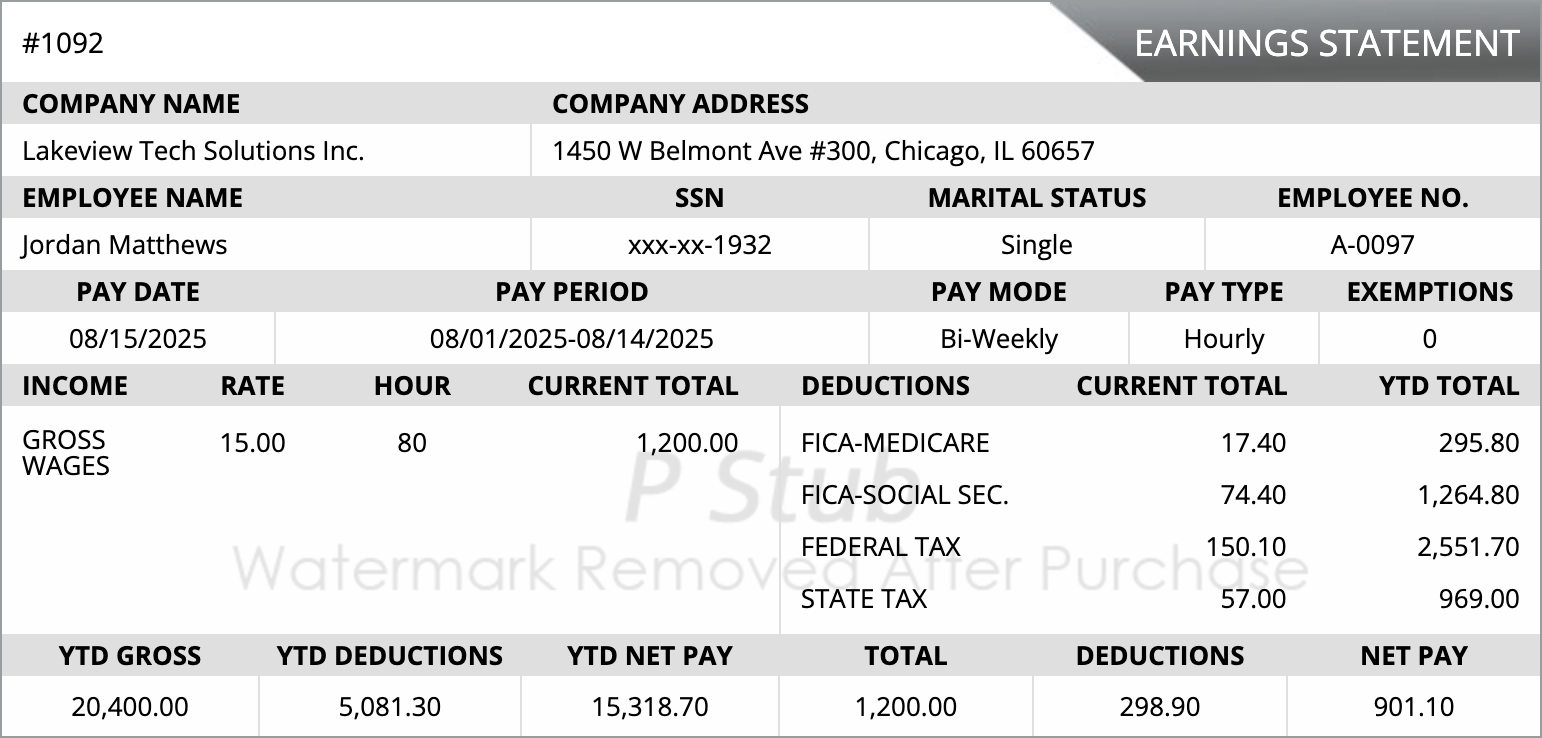

Overview of Payroll Cards

A payroll cards guide helps employers and employees understand what payroll cards are and how they work. Payroll cards are prepaid cards onto which employers load wages instead of issuing paper checks or direct deposits.

How Payroll Cards Work

When an employee opts for a payroll card, the employer loads the card with the employee's net pay each pay period. The employee can then use the card to make purchases, withdraw cash, or pay bills just like a debit card.

- Employees receive payroll funds automatically on payday

- No bank account is required to use a payroll card

- Funds are accessible at ATMs or point-of-sale terminals

Benefits of Payroll Cards

- No need for traditional bank accounts

- Fast access to wages on payday

- Reduced paper check costs for employers

- Convenient for employees without bank accounts

Considerations and Risks

While payroll cards offer convenience, there are some important factors to consider.

- Some cards may have fees for ATM withdrawals or balance inquiries

- Employees must understand fee structures

- State laws may govern payroll card usage and fee limits

- Training and education may be needed for employees unfamiliar with prepaid cards

Frequently Asked Questions

What is a payroll card?

A payroll card is a prepaid card onto which employers load an employee's wages for electronic access to pay.

Can employees use payroll cards without a bank account?

Yes, one advantage of payroll cards is that they do not require a traditional bank account.

Are there fees associated with payroll cards?

Some payroll cards charge fees for certain services, such as ATM withdrawals or customer service calls.

How do employees withdraw funds from a payroll card?

Employees can withdraw funds at ATMs or use the card for purchases wherever debit cards are accepted.

Understand Your Payroll Card Options

Use this payroll cards guide to decide whether payroll cards are the right option for your business and your employees.

Cookies Settings

Cookies Settings Reject All

Reject All Accept All Cookies

Accept All Cookies

Save & Close

Save & Close