Why Banks Verify Pay Stubs

Banks verify pay stubs to confirm that a borrower has a stable and legitimate income before approving financial applications such as loans, credit cards, or rental agreements. Income verification helps lenders evaluate whether an applicant can reliably repay borrowed money.

Pay stubs provide details about salary, deductions, and year-to-date earnings. However, lenders rarely rely on these documents alone. Instead, they cross-check the information with multiple financial records to confirm accuracy and prevent fraud.

The verification process protects both lenders and borrowers by ensuring that financial decisions are based on real and verifiable income data.

Initial Document Review

The first step banks take is reviewing the pay stub itself. Financial institutions carefully examine formatting, employer details, and payroll calculations.

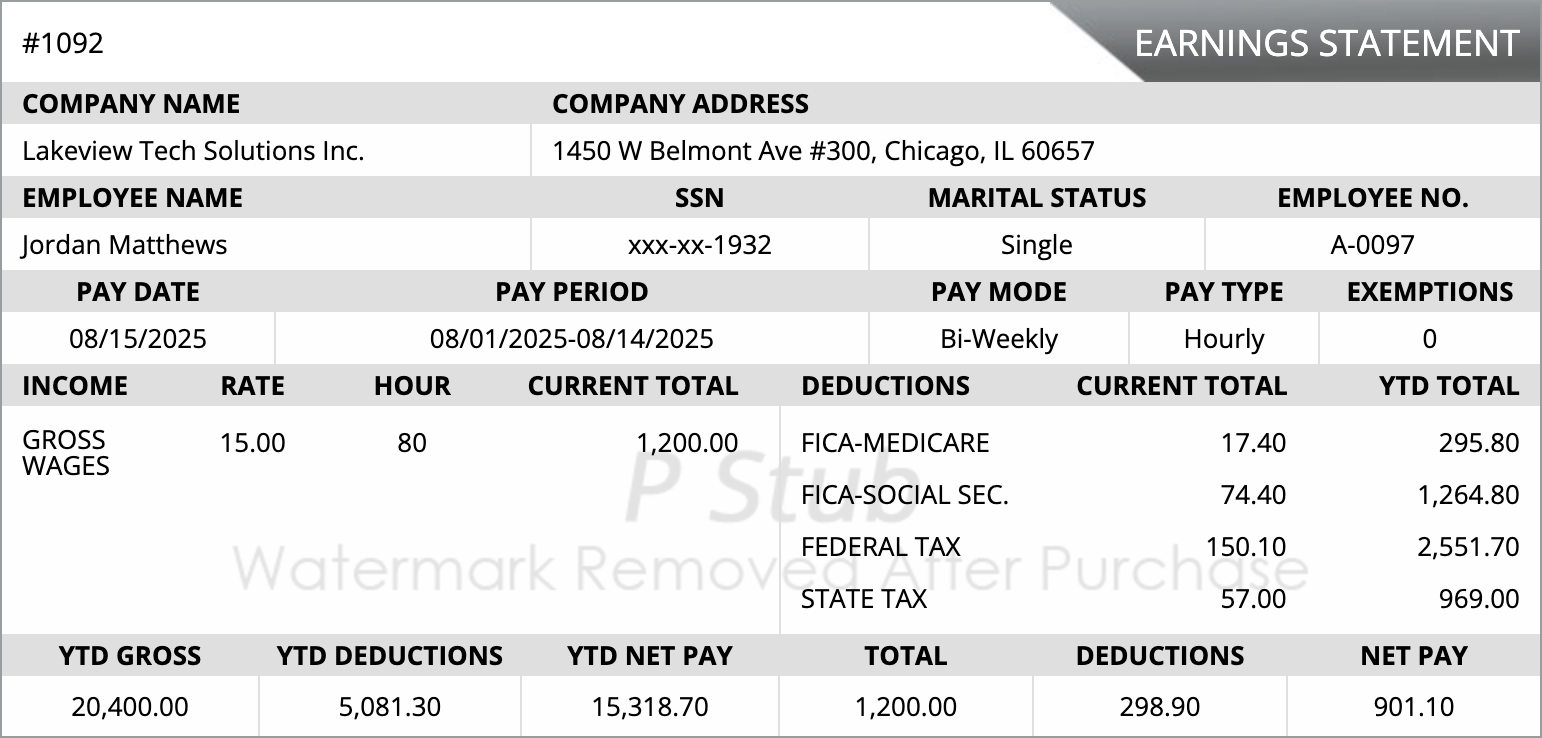

A legitimate pay stub typically includes:

- Employee name and identification information

- Employer name and contact details

- Pay period dates

- Gross income and net income

- Taxes and payroll deductions

- Year-to-date earnings totals

Underwriters often review the mathematical accuracy of payroll figures. If the gross pay minus deductions does not match the net pay shown on the document, it may indicate an altered or fabricated pay stub.

Employer Verification

Another common step in the verification process is confirming employment directly with the employer. Banks may contact a company's human resources department to verify the employee's position, salary, and employment status.

This verification can occur in two ways:

- Verbal verification through a phone call to the employer

- Written verification through official employment forms

The goal of this step is to confirm that the individual is actively employed and earning the income shown on the submitted pay stubs.

Bank Deposit Matching

Banks frequently compare pay stubs with bank statements to verify income consistency. They review direct deposit transactions and match them with the net pay listed on the pay stub.

If the pay stub indicates a biweekly income, for example, lenders expect to see consistent deposits in the applicant's bank account that match the same payment schedule.

Any significant discrepancies between pay stub earnings and actual deposits can trigger additional review or requests for further documentation.

Tax Record Verification

For larger financial transactions such as mortgages, lenders may request tax documentation to validate income history. These documents can include W-2 forms, tax returns, or official tax transcripts.

Tax records provide a long-term income history and allow lenders to compare current pay stubs with previously reported earnings. This helps ensure the borrower has stable income over time.

If the income reported on a pay stub differs significantly from tax records, lenders may request additional clarification before approving the application.

Common Red Flags Banks Look For

Banks and lenders are trained to detect suspicious details that could indicate a falsified document.

Some common warning signs include:

- Inconsistent fonts or formatting

- Missing employer contact information

- Rounded or unrealistic income figures

- Incorrect payroll calculations

- Pay periods that do not match the deposit schedule

When red flags appear, lenders typically request additional documentation to verify the applicant's financial information.

Frequently Asked Questions

Do banks always verify pay stubs?

Yes. Most banks verify pay stubs during loan or credit applications to confirm the applicant's income and employment status.

How many pay stubs do lenders usually require?

Many lenders request the two most recent pay stubs covering approximately 30 days of income history.

Can banks contact employers to verify income?

Yes. Banks may contact an employer's human resources department to confirm employment status and salary details.

What happens if a pay stub cannot be verified?

If a pay stub cannot be verified, lenders may request additional proof of income such as tax returns, bank statements, or employment verification documents.

Understanding Pay Stub Verification

Understanding how banks verify pay stubs helps applicants prepare accurate financial documentation. Providing complete and consistent records can speed up the approval process and reduce the chances of delays.

Accurate payroll documentation also strengthens financial credibility when applying for loans, housing, or other financial services.

Cookies Settings

Cookies Settings Reject All

Reject All Accept All Cookies

Accept All Cookies

Save & Close

Save & Close